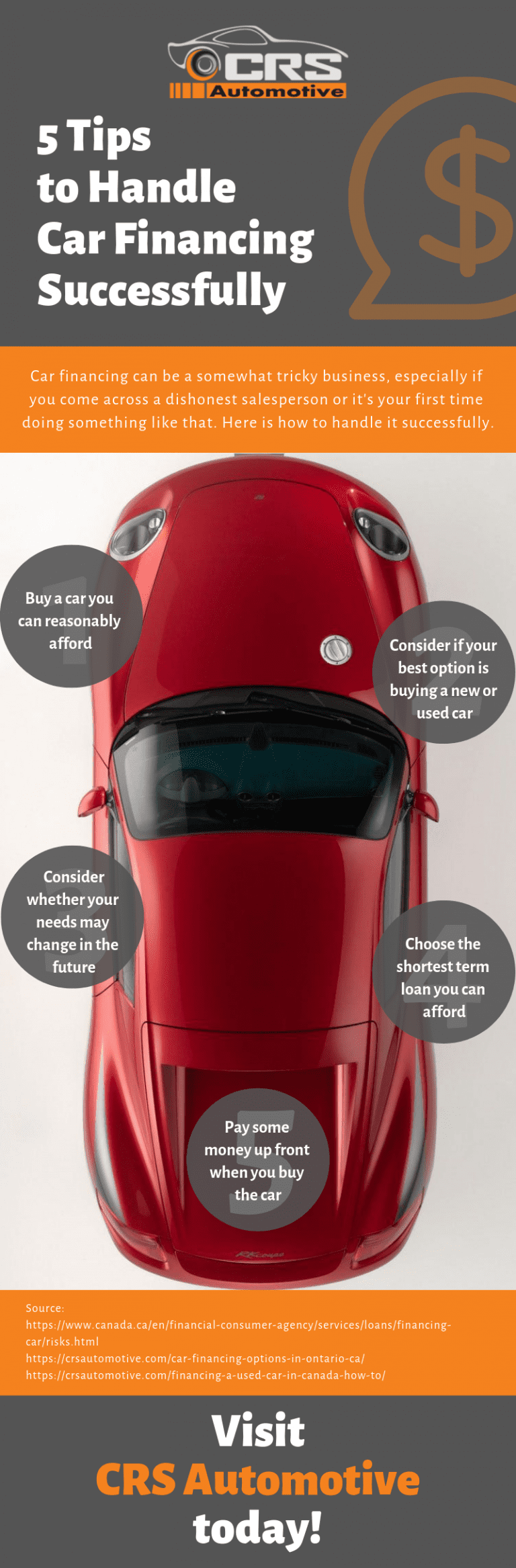

Getting a car financing can be a daunting task, especially if you’re a first-time buyer. But by following a few simple tips, you can make the process easier and ensure that you get the best deal possible.

There are several things to keep in mind when shopping for car financing. First, you need to determine how much you can afford to spend each month on your car payment. This will help you narrow down your search to cars that fit your budget. Second, you need to shop around for different financing options. There are many lenders out there, so it’s important to compare interest rates and terms before you decide on a loan.

Once you’ve done your research, you’re ready to start negotiating with lenders. Remember, you’re in control of the process, so don’t be afraid to walk away from a deal if you’re not happy with the terms. By following these tips, you can get the car financing you need at a price you can afford.

Car Financing Tips

Get pre-approved for a loan. This will give you a better idea of how much you can afford to spend on a car and will make the buying process go more smoothly.

- Shop around for the best interest rate. Don’t just accept the first offer you get. Compare interest rates from multiple lenders to find the best deal. (continue up to 2 point item)

Consider a shorter loan term. This will mean higher monthly payments, but you’ll pay less interest overall. If you can afford it, a shorter loan term is a good way to save money.

Shop around for the best interest rate. Don’t just accept the first offer you get. Compare interest rates from multiple lenders to find the best deal.

Interest rates can vary significantly from one lender to another, so it’s important to shop around to find the best rate. Even a small difference in interest rate can save you a lot of money over the life of your loan.

- Get quotes from multiple lenders.

Don’t just rely on your bank or credit union. Get quotes from online lenders, credit unions, and other financial institutions. You can also use a car loan comparison website to get quotes from multiple lenders at once.

- Compare the APR, not just the interest rate.

The APR (annual percentage rate) is the true cost of your loan, including the interest rate and any fees. When comparing interest rates, always compare the APRs, not just the interest rates.

- Consider your credit score.

Your credit score will affect the interest rate you qualify for. If you have a good credit score, you’ll be able to get a lower interest rate. If you have a poor credit score, you may need to pay a higher interest rate.

- Negotiate your interest rate.

Once you’ve found a lender you want to work with, don’t be afraid to negotiate your interest rate. Lenders are often willing to lower their rates if you ask.

By shopping around for the best interest rate, you can save a lot of money on your car loan.

FAQ

Here are some frequently asked questions about car financing tips:

Question 1: How can I get the best interest rate on my car loan?

Answer 1: Shop around and compare interest rates from multiple lenders. Consider your credit score and negotiate your interest rate with the lender.

Question 2: What is the difference between an APR and an interest rate?

Answer 2: The APR (annual percentage rate) is the true cost of your loan, including the interest rate and any fees. The interest rate is just the cost of borrowing the money.

Question 3: What is a good credit score for getting a car loan?

Answer 3: A good credit score for getting a car loan is generally considered to be 670 or higher. However, you may be able to get a loan with a lower credit score, but you may have to pay a higher interest rate.

Question 4: How much of a down payment should I make on my car loan?

Answer 4: The larger your down payment, the lower your monthly payments will be. However, you don’t need to make a large down payment to get a car loan. Some lenders offer loans with no down payment required.

Question 5: Should I get a new or used car?

Answer 5: New cars are more expensive than used cars, but they come with a warranty and the latest features. Used cars are less expensive, but they may not have a warranty and they may not have the latest features.

Question 6: How long should my car loan term be?

Answer 6: The shorter your loan term, the higher your monthly payments will be, but you’ll pay less interest overall. The longer your loan term, the lower your monthly payments will be, but you’ll pay more interest overall.

Closing Paragraph for FAQ: These are just a few of the most frequently asked questions about car financing. If you have any other questions, be sure to talk to a lender or financial advisor.

Once you’ve done your research and compared interest rates, you’re ready to start negotiating with lenders. Remember, you’re in control of the process, so don’t be afraid to walk away from a deal if you’re not happy with the terms.

Tips

Here are some practical tips for getting the best car financing deal:

Tip 1: Improve your credit score before applying for a loan.

The higher your credit score, the lower your interest rate will be. There are a number of things you can do to improve your credit score, such as paying your bills on time, reducing your debt, and getting a credit builder loan.

Tip 2: Get pre-approved for a loan before you start shopping for a car.

This will give you a better idea of how much you can afford to spend on a car and will make the buying process go more smoothly. You can get pre-approved for a loan online or at a bank or credit union.

Tip 3: Shop around for the best interest rate.

Don’t just accept the first offer you get. Compare interest rates from multiple lenders to find the best deal. You can use a car loan comparison website to get quotes from multiple lenders at once.

Tip 4: Consider a shorter loan term.

This will mean higher monthly payments, but you’ll pay less interest overall. If you can afford it, a shorter loan term is a good way to save money.

Closing Paragraph for Tips: By following these tips, you can get the best car financing deal possible and save money on your new car.

Once you’ve found a lender and negotiated a loan, you’re ready to sign the paperwork and drive off in your new car. Be sure to read the loan agreement carefully before you sign it.

Conclusion

Getting a car loan can be a daunting task, but by following a few simple tips, you can make the process easier and ensure that you get the best deal possible.

Here are the main points to remember:

- Shop around for the best interest rate. Don’t just accept the first offer you get. Compare interest rates from multiple lenders to find the best deal.

- Consider a shorter loan term. This will mean higher monthly payments, but you’ll pay less interest overall. If you can afford it, a shorter loan term is a good way to save money.

- Make a larger down payment. The larger your down payment, the lower your monthly payments will be. If you can afford it, make a down payment of at least 20% of the car’s purchase price.

- Improve your credit score before applying for a loan. The higher your credit score, the lower your interest rate will be. There are a number of things you can do to improve your credit score, such as paying your bills on time, reducing your debt, and getting a credit builder loan.

Closing Message: By following these tips, you can get the best car financing deal possible and save money on your new car. Be sure to read the loan agreement carefully before you sign it and make sure you understand all of the terms and conditions.